Netflix faces a new challenge in streaming: It is the high-priced player in a crowded market. One solution would be for the company to acquire another player, such as ViacomCBS, giving it another streaming brand with a lower-priced offering and with exposure to the ad market.

2 February 2022 (Malta) – Today I finished my first monograph of the year, a look at the streaming industry. The full monograph is only available to my select media client ba$e (see what I did there?) but I wanted to share a few points with those readers who have expressed an interest in following my media posts. For this post, a few words about Netflix.

BEGINNINGS

In 2016 I had the opportunity to meet with several members of the Netflix management team and IT team at the Mobile World Congress. At the time Netflix announced it was going live in 130 new countries. The list included massive new audiences like Russia, India, and South Korea. It was a huge expansion of the company’s footprint, with China the notable exception to major markets where you can now stream its content. It in effect tripled its distribution. What you had was the birth of a new global internet TV network.

But I was more fascinated by the “code” behind all of this and my team and I received lots of briefing sessions. Yes, Netflix is known as a place to binge watch television, but behind the scenes there’s a lot that goes on before everyone’s favorite show can be streamed. The process of building code to ramp up capacity utilization, scale and managing multi-region deployments is an awesome thing. It is a Master Class in understanding the physical components of cloud infrastructure, networking equipment, servers, data storage, hardware abstraction layers, the virtualization of resources and a host of other technologies.

In 2019 I had the opportunity to make a presentation on Netflix at a Disney Research Center media event in Zurich.

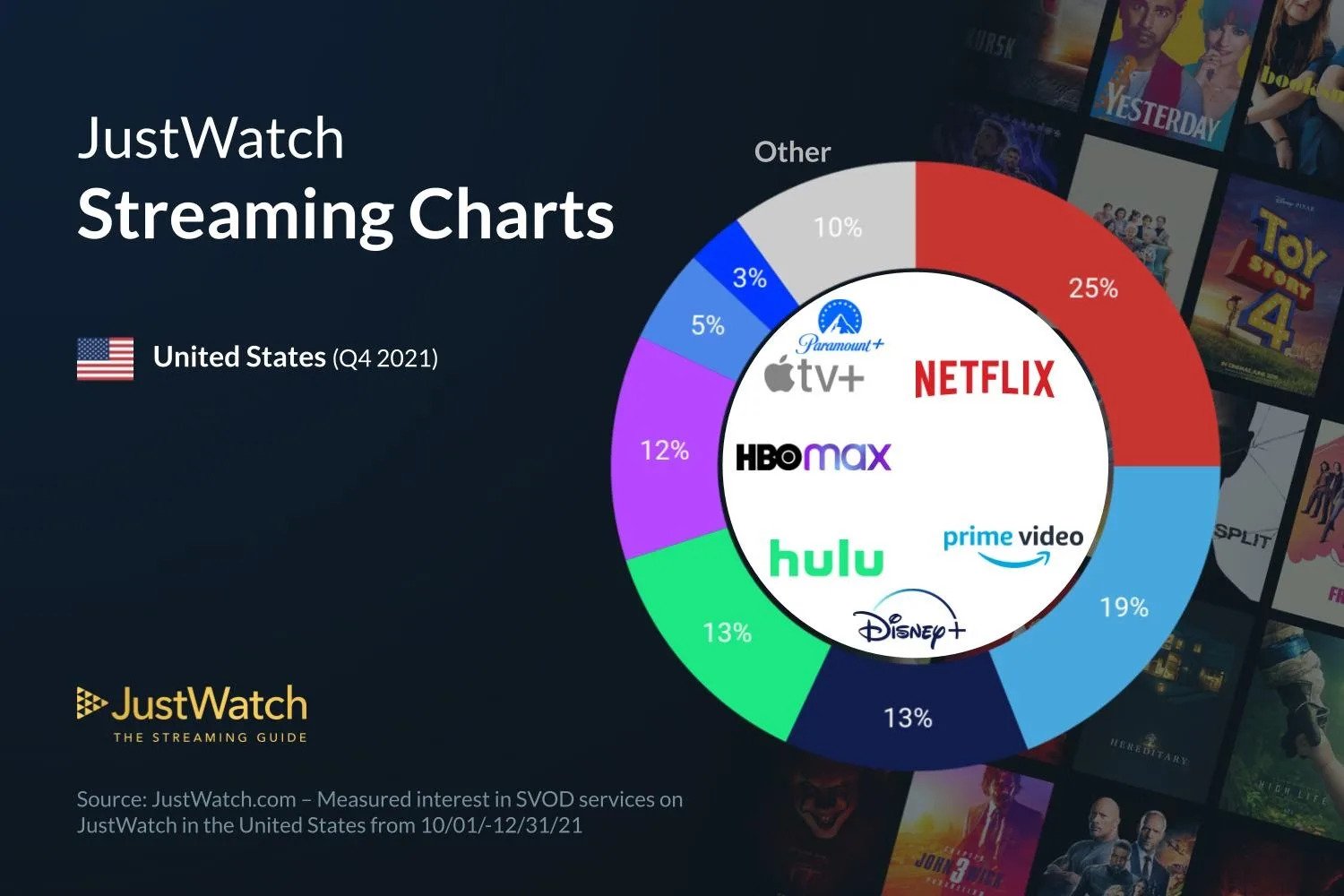

Netflix is now a well-entrenched member of the FAANG stocks … Facebook, Amazon, Apple, Netflix, and Google … a phrase that didn’t even exist in the Steve Jobs era. Netflix alone accounts for over 14% of the total downstream volume of traffic across the entire internet and just over 12% of all internet traffic. But it accounts for over 40% of downstream traffic in the peak evening hours.

BUT ALL IS NOT WELL

In its last report to stockholders, if Netflix’s warning of sharply slower subscriber growth tells us anything, it’s that Reed Hastings needs a new formula. The Netflix co-founder built the company into the leading video-streaming firm with a low-priced offering in a new market. But Netflix is now the priciest offering in an extremely crowded market. Without a change in tactics, Netflix risks becoming a slow-growing company that produces little in the way of cash—a fatal combination from an investment standpoint. To avoid that scenario, Hastings could break the mold and pursue a big acquisition, buying a rival TV company such as Paramount+ owner ViacomCBS. That would give Netflix an additional brand that offers lower-priced tiers of service, one of which carries ads, thereby diversifying its revenue.

An offering like that would make it easier for Netflix to attract consumers who don’t want to pay the minimum $10 a month cost for its service. That’s twice as much as the lowest tier of other big-name services, such as Discovery+, Peacock, Apple TV+ and Paramount+. Such a move would also help consolidate the now-crowded market, including internationally, where most of the U.S. companies are now competing. That would give Netflix more pricing power.

Netflix bulls will argue such a move isn’t necessary. In their view, the current slowdown in growth is a temporary lull related to distortions produced by the pandemic – that’s certainly what Netflix executives seem to think, judging by comments on the fourth-quarter earnings call a couple of weeks ago.

“The slowdown is probably a bit of just overall Covid overhang that’s still happening after two years of a global pandemic,” said Chief Financial Officer Spencer Neumann.

The company’s advocates might be right. Netflix has become synonymous with streaming, and offers a deep array of programming. The stock has since bounced from a low of around $360 to Tuesday’s close of $457.13.

But Netflix is far from cheap, particularly at its current levels, given that analysts expect revenue growth of just 12% to 13% annually in the next couple of years, according to S&P Global Market Intelligence. Most companies growing at that leisurely pace generate lots of cash which can be used to pay dividends and buy back stock: Netflix over the past few years has mostly burned cash. The company said last month, however, that it anticipates “being free cash flow positive for the full year 2022 and beyond.”

Certainly compared to its older TV rivals, Netflix still retains a hefty premium. The stock is currently trading at 6.4 times next year’s revenue, according to S&P, while ViacomCBS, Discovery and Disney are trading between 1.3 and 3.8 times. The trio is growing even more slowly than Netflix, for sure, but they also generate significant amounts of cash. Discovery, for instance, generated $2.3 billion in free cash flow in 2020. Its expansion in streaming will dampen that, for sure, but not wipe it out: analysts estimate that the company produced $2.1 billion in 2021.

LIMITS OF GROWTH

Netflix’s biggest growth challenge is likely the U.S. On the company’s recent earnings call, Hastings said Netflix had now reached about two-thirds of pay TV’s “high-water mark” of subscribers in the U.S., implying the company had about 66 million subscribers there. (Netflix discloses North American numbers but not the U.S. alone). Hastings said signing up the “back third is definitely going to be harder than the first two-thirds.” He added that because Netflix doesn’t offer either sports or news, “if we get to 80% or something of pay TV, that’s a good accomplishment.”

What he didn’t acknowledge is how much the market has shifted since Netflix launched its streaming service more than a dozen years ago. Then, Netflix was almost alone in the field, and its service was a great deal compared with cable TV. Netflix charged $8 a month for its first pure streaming service, which it introduced in late 2010. That compared with the $75 a month or so the average household paid for cable.

At that time, Netflix’s only real competition was streaming service Hulu. Amazon jumped into the market soon after with its Prime Video service. Today, Apple and almost every TV firm, from Discovery to Disney, has jumped into the market with robust streaming offerings. And those are just the big-name services. Lots of smaller, niche services have become available over time, including some free ad-supported offerings. A report by S&P’s Kagan unit earlier this week identified at least 141 streaming services launched between 2011 and 2021, compared with 18 between 2005 and 2010.

Of the major services, Netflix is now the high-priced competitor. Its middle tier costs $15.49 a month. Every other service offered by major companies is cheaper. Disney, for instance, offers a bundle of Disney+, Hulu and ESPN+ for less than that.

All the TV companies offer video-streaming services with cheap ad-supported tiers in addition to more expensive ad-free tiers. On a call with analysts last week, Comcast CEO Brian Roberts said its research showed that 80% of people preferred an ad-supported service over a more expensive, ad-free one.

Hastings has repeatedly ruled out introducing ads to Netflix, however, largely on the basis that it would entail “exploiting users” by using data to allow for targeted advertising. But in doing so, Netflix is limiting its ability to offer consumers a cheaper version.

INTERNATIONAL CHALLENGES

In recent years, Netflix has driven the vast majority of its subscriber growth internationally. That remains its biggest opportunity. But it is already strong in Europe, where it now faces competition from all the other U.S. firms. Where it lags is in markets like India where Amazon has done better. After fumbling the market by overcharging, Netflix recently cut prices in an effort to jump-start growth.

The problem with subscriber growth in countries like India, however, is that Netflix might add millions more subscribers but at a fraction of the revenue.That’s the issue Disney has encountered: Much of the growth in Disney+ has been coming from India, where the service’s average price is a fraction of what it generates overseas. With subscriber growth likely constrained, and Netflix’s ability to raise prices also limited, it’s hard to see top-line growth accelerating. What about Netflix’s ability to generate more cash? Its statement that it would generate free cash flow this year signals the years of rapid growth in program spending, which caused the company to burn through billions a year, are over.

Generating significant free cash flow is another story. Last year Netflix burned through $159 million in cash on $29.7 billion in revenue, thanks to $17.5 billion spent on programming. In the future, either revenue has to grow significantly while programming stays constant, or program spending has to be reduced. Cutting program spending may not be appealing, given the risk that Netflix will lose subscribers. As The Wall Street Journal noted in a report earlier this week, data shows that for all the streaming services, hit shows bring in new subscribers who quickly cancel.

CULLING THE MARKET

This leaves consolidation as Netflix’s best hope. At some point in the next couple of years, some of the big TV companies whose services are lagging will likely give up, reducing competition for both programming and customers. That will give those that remain more pricing power. Netflix could try to speed up the process by buying an existing company. ViacomCBS is one option. Netflix might be able to snap it up for around $40 billion, including debt. Netflix could easily absorb that, given its $202 billion market cap.

By adding ViacomCBS’ Paramount+, Netflix could get the benefit of a lower-priced rival, one with ads, to reach a broader audience. Netflix could introduce its own lower-priced, ad-supported tier but that might dilute the value of the Netflix brand and undercut Hastings’ promises to not introduce ads. In buying ViacomCBS, Netflix would also get ownership of Paramount Pictures, which, with its library of older shows, could guarantee access to those reruns in the long term. Nielsen data shows that TV network reruns continue to draw sizable audiences for Netflix.

Whatever direction Netflix goes, it can’t just stick with the same old formula. The streaming market has evolved and Netflix needs to evolve with it.